There is no way to sugar coat the human misery entailed in the Russian invasion of Ukraine but let me try to offer a purely economic perspective of the potential impact on the world economy. We see from the rise in oil prices to over $100 a barrel that a disruption in energy supplies to Europe will lead to higher inflation and weaker growth than earlier projected by economists.

There is no way to sugar coat the human misery entailed in the Russian invasion of Ukraine but let me try to offer a purely economic perspective of the potential impact on the world economy. We see from the rise in oil prices to over $100 a barrel that a disruption in energy supplies to Europe will lead to higher inflation and weaker growth than earlier projected by economists.

This will make for a very delicate balance for central banks here and abroad. We see already that US yields are dropping as money flows from the markets to the safe haven of treasuries. This may well lead to a slower increase in the discount rate than recently expected which will help growth stocks that are very sensitive to interest rates bounce back after the crisis.

Historically, there is the old saying that you “buy on the invasion” when these type of geopolitical events occur, but every situation is different. We will most certainly be in for a period of higher volatility and this is actually a positive opportunity for investors with a long-term time horizon.

Balance sheets and cash flows are strong for most industries due to the near zero interest rates in the past decade. This pull back may well offer some very attractive merger and acquisition opportunities for corporations and the banking sector should benefit from this activity.

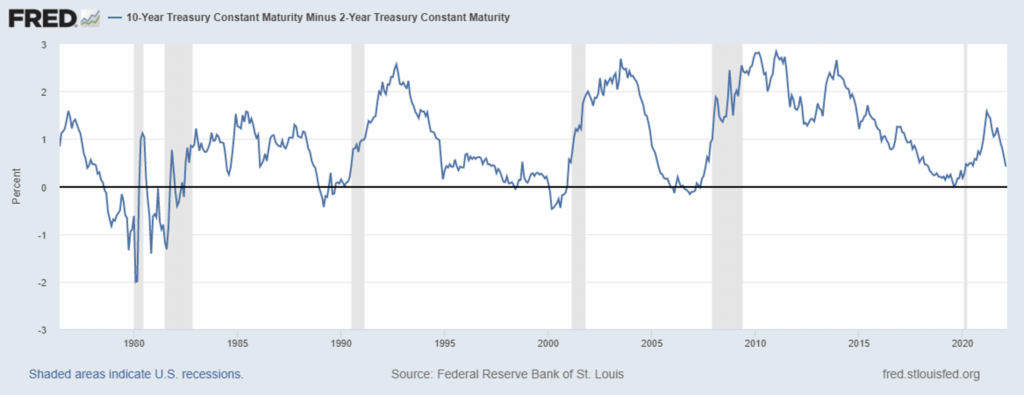

The graph below shows the widely followed 10 year minus the 2 year treasury yield curve. You can see that it has been flattening in recent months which often leads to an inverted yield curve. Many times an inverted yield curve, where short term rates are higher than long term rates, is a precursor to a recession (the shaded areas on the graph).

The federal funds rate is the target interest rate set by the Federal Open Market Committee (FOMC). This is the rate the Federal Reserve (FED) charges for overnight lending between commercial banks. Through this rate the Fed is able to influence short term rates on consumer loans and credit cards.

The rate has been at 0.25% since March of 2020 at the start of the Covid pandemic. With the current rate of inflation hovering at 7% economists have widely expected the Fed to raise this target rate by 0.25% seven times this year which would get it to 2.0%. With the Russian invasion of Ukraine the Fed may need to reduce the number of increases in the rate to only three or four times this year. This would leave the short term target rate at 1 – 1.25% and would stop the flattening of the yield curve. That is a positive for growth and value firms coming out of this conflict.

In conclusion, it is reasonable to expect considerable volatility in the coming weeks and months. We will likely see cyberattacks and additional sanctions on Russia but do not forget that long term investors should not panic sell. In fact, if you have idle cash to invest this is the time to start working with your advisor to put together a well-thought out plan based on your level of risk tolerance and financial situation.

Content in this material is for general information only and not intended to provide specific advice or recommendations for any individual. All performance referenced is historical and is no guarantee of future results. All indices are unmanaged and may not be invested into directly.

All investing involves risk including loss of principal. No strategy assures success or protects agains loss. Because of their narrow focus, sector investing will be subject to greater volatility than investing more broadly across many sectors and companies.

March 2022